Gen Z, C2C and new competition redefining the CEP landscape in 2025

How shifting end-consumer behaviour and new delivery models are pushing CEP operators to rethink visibility, flexibility and fulfilment.

How shifting end-consumer behaviour and new delivery models are pushing CEP operators to rethink visibility, flexibility and fulfilment.

Disclaimer: This text was originally written in English and translated using AI.

The CEP industry has never operated in a more complex environment. Higher expectations, tighter margins, rising ESG demands and unprecedented competition in the Last Mile are reshaping what end-consumers expect – and how operators must respond.

The 2025 Geopost E-Shopper Barometer shows that Gen Z is the most active online shopper, making more than 60 online purchases per person each year. Yet they are also the hardest generation to satisfy: only three in ten say they are happy with their delivery experience.

Gen Zs expect transparency, real-time tracking, convenience and ESG-friendly options – even if most shoppers still place price first.

Nevertheless, the Barometer does show that a growing number of Gen Z end-consumers are willing to accept slower delivery or pay a small premium for environmentally-friendly choices.

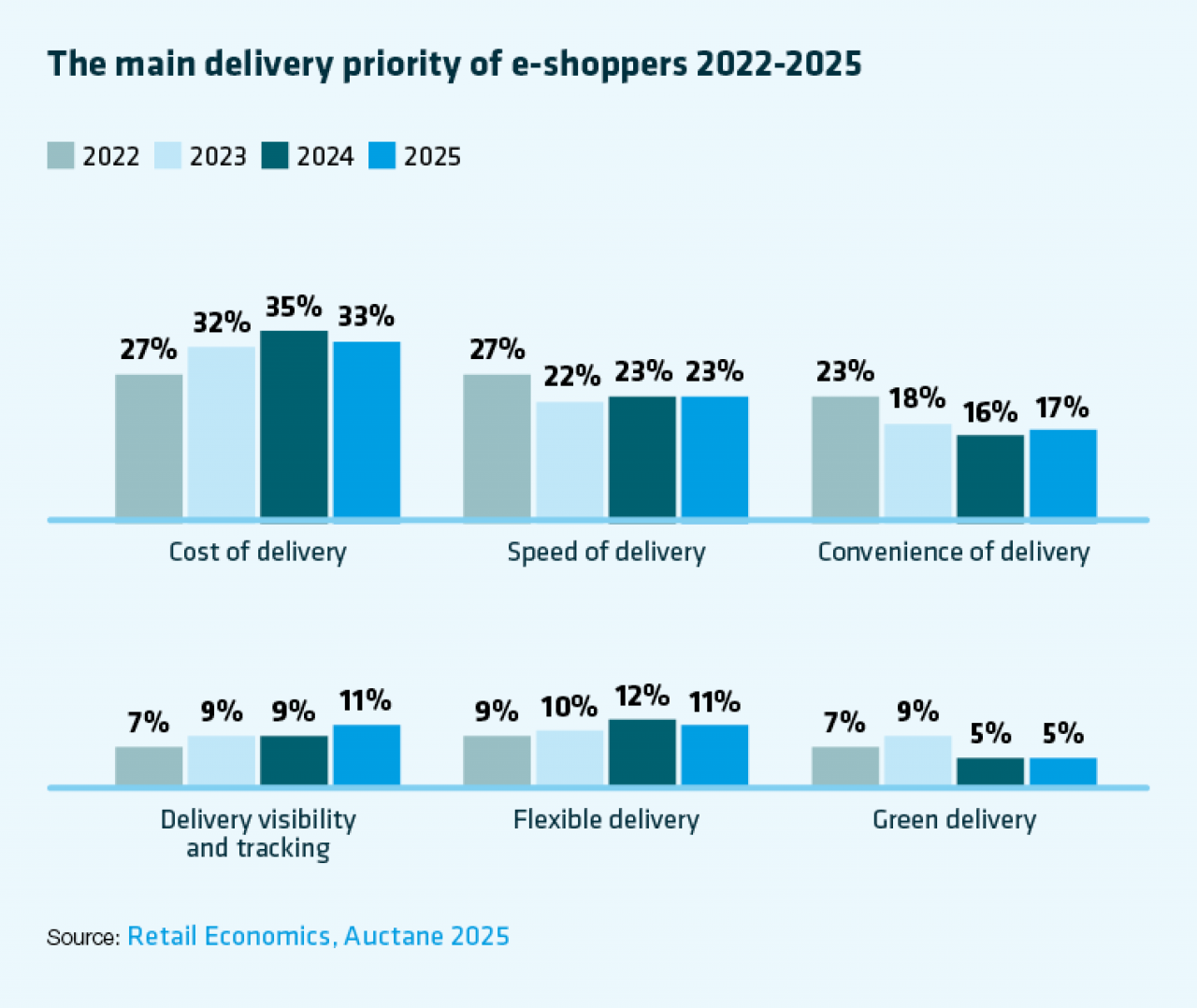

Recent data from Retail Economics and Auctane offers additional context for e-shoppers in general. While cost still dominates delivery preferences, demand for better visibility, real-time tracking and more flexible options is steadily rising. This reflects a broader shift: consumers increasingly want greater control over how and when parcels arrive.

To explore the data behind Gen Z’s rising expectations and the main delivery priorities of e-shoppers overall, download the full report here.

Two behavioural shifts are transforming demand patterns across the parcel network:

Some 96% of Gen Z say social media influences their purchases, and 61% buy directly within platforms. This accelerates expectations for fast, visible and highly flexible delivery options.

As many as 72% of regular e-shoppers now use C2C platforms. As buying and selling behaviours intensify, demand grows for out-of-home (OOH) solutions – especially parcel lockers and PUDOs – which offer affordability and convenience for both buyers and sellers.

These aren’t temporary trends. They are reshaping when, where and how parcels move through the Last Mile.

The rapid expansion of gig delivery operators such as Deliveroo, Wolt and Glovo is reshaping the competitive landscape. Once focused on providing takeaway food services, they now deliver groceries, retail goods and even pharmaceutical items, using dense, hyperlocal networks to provide fast, flexible urban fulfilment.

Although many face regulatory and financial headwinds, their influence on delivery expectations is undeniable.

For traditional CEPs, this adds yet another layer of competition in an already stretched market. At the same time, the instability of gig platforms creates opportunities for CEPs to differentiate through reliability, compliance and end-to-end fulfilment services that gig couriers cannot match.

Retailers are increasingly looking for delivery partners who can support reverse logistics, 3PL services and integrated fulfilment, not just traditional parcel transport.

Operators such as PostNL, bpost and Australia Post have already begun this transition, signalling a broader industry shift toward more embedded, value-added service models.

The message from the Beumer Group CEP 2026 Outlook is clear: Gen Z expectations, C2C growth, social commerce and gig economy competition are reshaping the CEP market.

But these shifts also create openings for operators ready to innovate around visibility, delivery choice, fulfilment integration and sustainable operations.

Get the complete analysis in BEUMER Group’s CEP 2026 Outlook, ‘The interconnected challenges’.