2021 e-commerce trends for the CEP industry

Before 2020, the CEP industry had already been in a state of disruption for several years. The current surge in e-commerce is a major transformative trend.

Before 2020, the CEP industry had already been in a state of disruption for several years. The current surge in e-commerce is a major transformative trend.

Disclaimer: This text was originally written in English and translated using AI.

Before the events of 2020, the CEP industry had been undergoing a significant transformation.

In fact, it had already been in a state of disruption and uncertainty for several years. The key factor driving this transformation has been the surge in e-commerce and changing customer expectations – both B2B and B2C. Customers, both end-consumers and industrial, have come to expect to receive shipments faster, with more flexibility and at a lower price.

On the B2C side, new consumer shopping behaviour has been emerging. It has become apparent that online consumers don’t care who delivers their goods, as long as they receive them quickly, cheaply and reliably. Consumers have been increasingly seeking flexible delivery in terms of when and where they get their shopping items. Most have come to expect it free of charge and are only prepared to pay a premium for faster delivery and high-value items. Dynamic pricing for parcels has been deemed unacceptable – customers have expected to pay the same for shipping expenses, regardless of the season.

The B2B side has been no different. Industrial customers have been under strain in terms of operational efficiency, profitability and performance. They too have expected faster time-to-market, lower defect rates and customised products. Indeed, in some manufacturing industries, the pace of changing customer expectations has been even faster than that of the private end-consumer.

This has been due to the so-called ‘Industry 4.0’ and the arrival of the industrial Internet of Things. Whether it has been producers of consumer goods, cars, planes or industrial equipment, B2B customers have been forced to redefine how they interact with their customers and how they organise their supply chains. (Source: PwC)

This article is an excerpt of the report The State of Courier, Express and Parcel 2020 and Beyond – Challenges and Perspectives.

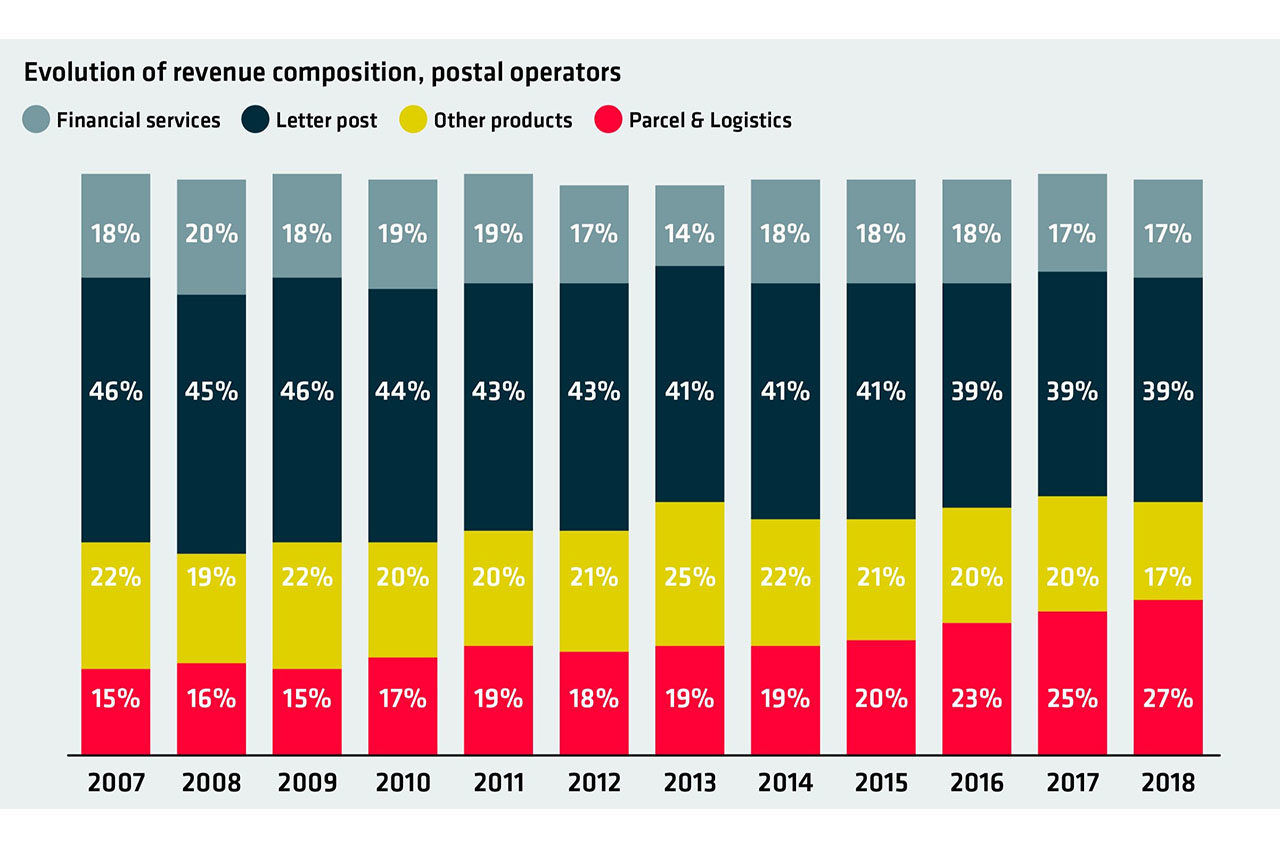

What has all this meant for the CEP industry? For most hubs and distribution centres, this increase in e-commerce has led to significant growth in the last six consecutive years. The jump in the share of parcel and logistics in total revenue for most hubs reflects this growth.

As the UPU reports, the share of letter post in the total revenues of postal operators dropped in the years 2008 to 2018, to the benefit of parcels and logistics, which jumped over the same period (see Figure 1). So, while CEP has represented a smaller segment in the larger logistics industry, it has been a fast-growing segment, with the major part of its market being linked to B2B transactions and a third of its revenues attributed to B2C. (Source: PwC)

Figure 1: Evolution of revenue composition, postal operators. (Source: UPU)

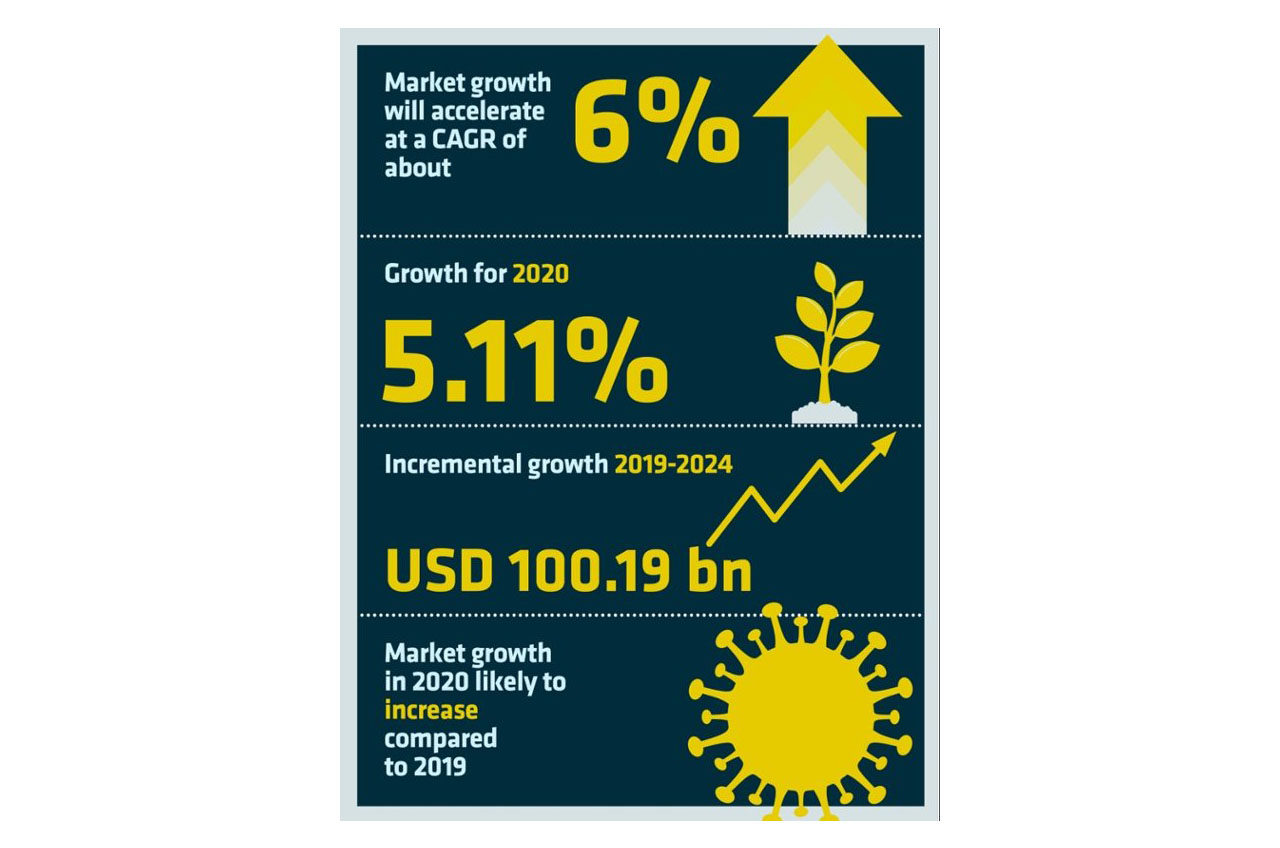

As a result of this growth, the CEP market is expected to reach USD 422.07 billion by 2024. Indeed, in July 2020, Businesswire reported that the CEP market is poised to grow by USD 100.19 billion during 2020-2024, progressing at a CAGR of about 6% during the forecast period. The value of the market was USD 321.88 billion in 2019.

At BEUMER Group, we’ve seen substantial growth over the last six years for both B2B and B2C and consider the projected growth figures to be sustainable, noting that the pandemic has had a big effect.

Even when Covid is brought under control, the change of attitude on the part of consumers and the pattern of consumer behaviour will be sustainable.

Figure 2: Growth of the CEP market. (Source: Technavio)

Clearly, the transformation of the CEP industry had been well underway before the impacts of the pandemic started to show. However, there can be no doubt that the pandemic has accelerated this transformation. Indeed, some experts say that the crisis has accelerated the development of online purchasing activity by nearly three years.

Even when Covid is brought under control, the change of attitude on the part of consumers and the pattern of consumer behaviour will be sustainable.

Where the consumer once had been averse to buying goods online, the pandemic’s impact has left consumers no other choice. Accenture’s Freight and Logistics division has predicted that even when events return to normal, such changes will be permanent. Customers will continue to buy more online and those who rarely bought online will make it a common channel.

The impact of the pandemic on the CEP industry, however, has not been uniform. While the projected growth figures are global, e-commerce growth will vary on a regional level. Those regions hit less severely, economically, will continue to experience success in their e-commerce development. However, some regions will be more fragile; protectionism and weak financial situations will damage this e-commerce expansion.

As different countries have different mixes across these segments and are subject to different macroeconomic and social contexts, the effects of the crisis may vary geographically.

The sustainability of the offset brought on by the pandemic may also vary according to market segments. While B2C shipment volumes have been very high (pre-Christmas peaks were felt in March, April and May 2020), B2B shipment volumes have declined significantly due to the slowdown in the economy. Early in the crisis, for example, Royal Mail UK experienced significant falls in B2B volume in some markets. These falls were not offset by higher consumer volumes.

Hence, those CEP providers serving B2B businesses may continue to see significant decreases in traffic whereas businesses with many B2C customers will not. As many providers service both sectors within their businesses, they may witness further growth on one level but decline on another.

Directors of CEP companies are going to have difficult decisions to make in how they reorganise their organisations.

Accordingly, even though overall e-commerce remains stable, there may be many internal fluctuations within different companies – and directors of CEP companies are going to have difficult decisions to make in how they reorganise their organisations.

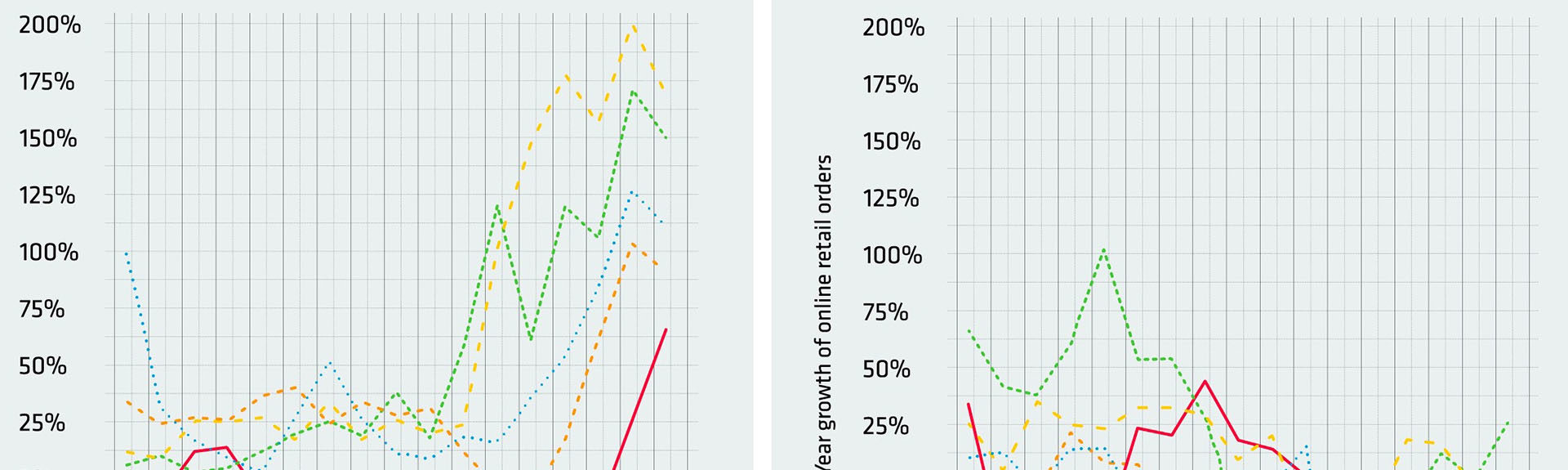

It’s clear that the global pandemic has impacted domestic parcel flows in various ways. This can be seen in evolving online retail orders which correlate to the demand for parcel post.

As the UPU reports, some countries have seen a strong increase in domestic online orders, while others have seen the same variable drop dramatically. Although the figure shows the trend for only ten countries, it would appear that e-commerce sales have increased in higher income countries, while stabilising or even dropping elsewhere.

Despite the pandemic and its variant impacts, CEP shipment volumes continue to rise. Take Germany, for example, where CEP shipment volumes are expected to rise to around 4.5 billion shipments by 2024.

For the CEP sector, this means that market vendors will be focusing more on growth prospects in fast-growing segments while maintaining their positions in slow-growing segments.

Businesses will be watching for patterns and changes and how they should shape strategies moving forward.

What this means for the CEP market is that certain players will want to grab this opportunity of growth. If they have the power to invest, these service providers will want to aim for volume. In turn, suppliers, such as BEUMER Group, will be in a strong position to harvest this demand for high capacity.

Certain players will want to grab this opportunity of growth. If they have the power to invest, these service providers will want to aim for volume.